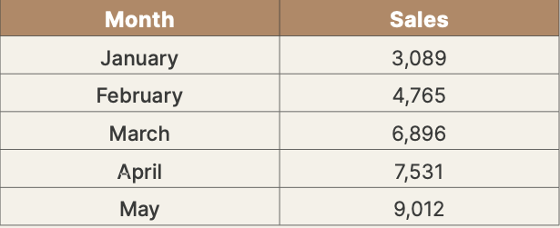

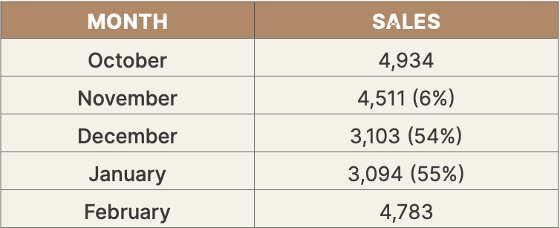

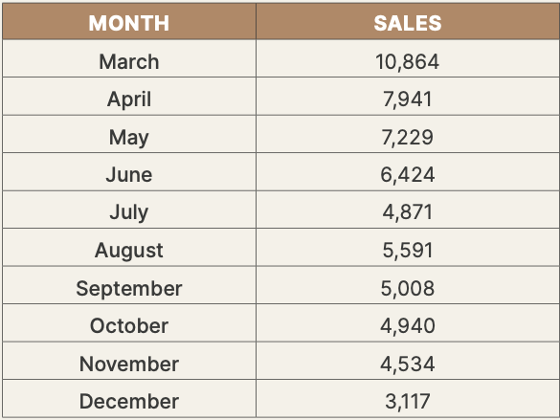

The Toronto and Region residential resale marketplace is, to say the least, confusing. The numbers reported by the Toronto Regional Real Estate Board depict a market in the doldrums with sales volumes having declined for 4 consecutive months, reaching levels more consistent with sales volumes achieved more than two decades ago when the greater Toronto area had a population almost half of what it has today.

Although there is some seasonality in these numbers, August and now September’s performance is low beyond any seasonal impact.

What we also see in September is a sharp increase in residential inventory. In September 16,258 homes became available for sale. This represents a 44.1 percent increase compared to the 11,281 properties that came to market last year. As we begin October buyers have 18,912 properties to choose from, almost a 40 percent increase compared to the mere 13,529 that were available to buyers last year. About 35 percent of the market’s active inventory is condominium apartments.

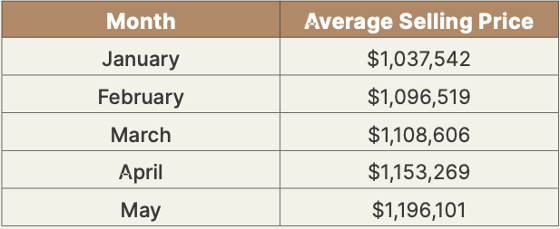

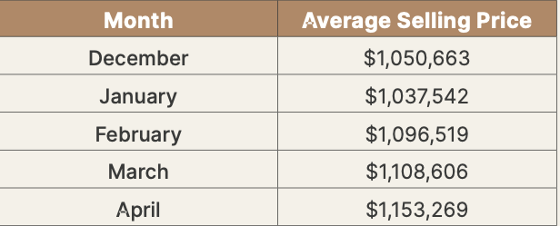

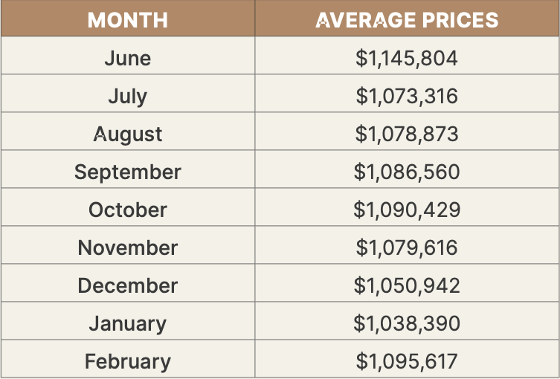

Historically this scenario, low sales volumes and dramatically increasing available inventory, would mean only one thing - falling average sale prices. But that is not what is happening. Surprisingly average sale prices are strengthening, notwithstanding that almost 40 percent of the available inventory is condominium apartments and townhouses.

In September the average sale price came in at $1,119,428, 3 percent higher than the average sale price achieved last September ($1,086,538). More significantly September’s average sale price for all properties sold (including condominium apartments and townhouses) was 3.5 percent higher than the average sale price of $1,082,569 achieved in August.

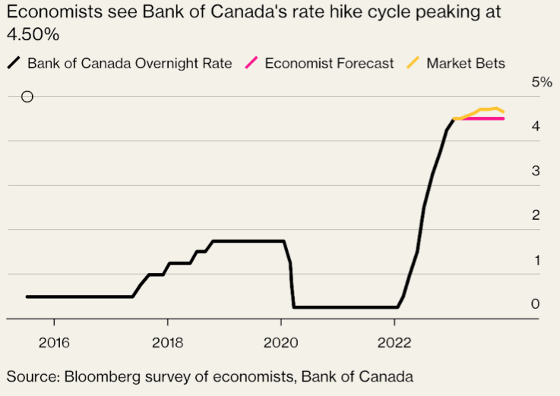

There is no precedent for these market conditions. No doubt because no market in the past has come through a pandemic, enormous government stimulus, inflation, and then a draconian monetary policy implemented by the Bank of Canada. Added to this incredible mix of extreme economic and social factors is soaring population growth driven by immigration. In 2022, Canada’s population grew by more than 1 million people, many finding their way to southern Ontario. Canada sent 17,145 new permanent residents and express entry draws in September alone (Immigration News Canada).

If we dig a little deeper into the numbers we see that detached and semi-detached properties are selling at a ferocious pace. All detached properties in the City of Toronto sold in a mere 16 days and at 101 percent of their asking price. The average sales price was $1,724,007. All semi-detached homes sold in an eye-popping 11 days at 106 percent of their asking price. The average sale price for all semi-detached properties reported sold was $1,281,956.

Not surprisingly condominium apartments did not move at the same pace. A typical condominium apartment took 25 days to sell and at only 99 percent of its asking price. The average price for all condominium apartments sold was $732,106. Based on the number of available condominium apartments in Toronto (4,539) and the number of reported sales (850), this equates to almost 5.5 months of inventory.

So what do we make of these numbers? Put simply it is a market of “haves and haves not”. Population growth has created demand. Supply, while growing, is still low, particularly in the detached and semi-detached sectors. Within the demand sector, there are those buyers who can, notwithstanding the prevailing high financing costs, afford to purchase detached and semi-detached properties that become available. They do so quickly and often pay over the asking price. Regretfully the number of buyers that fall into the “haves” is small, hence the declining monthly sales. Financing costs are turning most aspiring buyers into “haves not”. Most of the latter look to condominium apartments, the least expensive housing type available to buyers. That’s why condominium apartments are taking longer to sell and do so below their asking prices.

Dejardins recently completed a study of the prevailing resale market. It concluded that the market could go in one of three ways. An early 1990’s restructuring, with declining sales volumes and average sale prices over a protracted period of time. A mild recessionary market with average sale prices declining moderately by about 6 percent. Or a market in constant stress between supply and demand in the face of painful mortgage financing. In this market scenario sales would decline but prices will, because of the demand, continue to rise, albeit moderately.

It appears that we have entered the third market scenario. Early October numbers at least for now, to confirm this assessment.